Marine carbon removal: the binding constraint is verification, not chemistry or cost

A Steps Ventures thesis. Position and conflict of interest: Steps Ventures is an advisory firm, and this thesis is shaped by our own research, which is being submitted for peer review. We publish it to be argued with. Every number is traceable to an open data release.

Marine carbon removal is a real market with a physics problem the market has not priced. The prevailing way to screen ocean-CDR opportunities is on two axes: the chemistry of the site (how much carbon a given intervention should remove) and the cost per tonne. Our work says both are the wrong binding constraint. The binding constraint is verification, and whoever solves it captures the value.

Three findings drive the thesis.

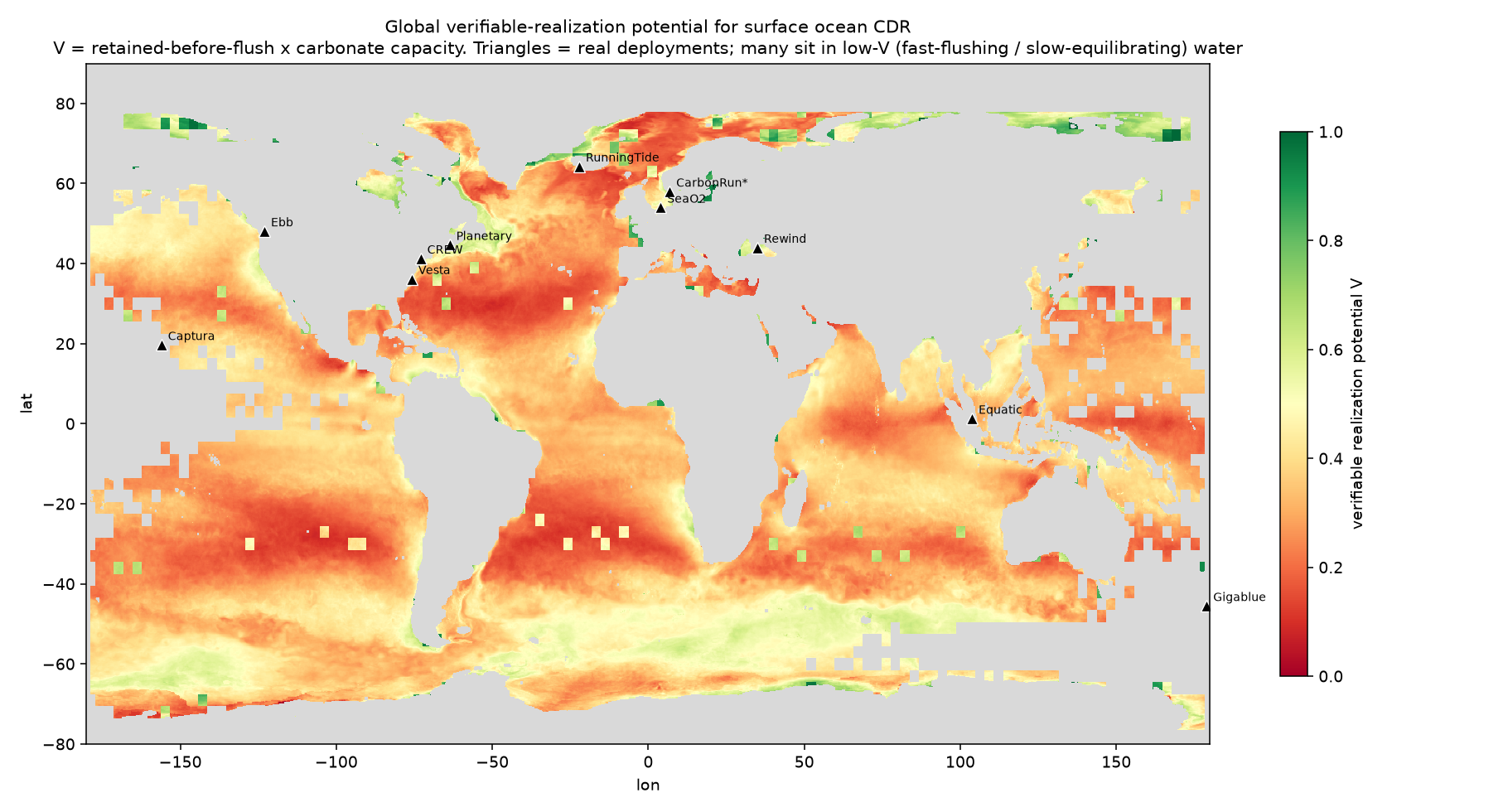

First, realized near-term removal is systematically lower than the efficiency atlases imply, and it is lowest at exactly the high-interest deployment regions. The atlases used to site and credit ocean alkalinity enhancement run at about 100 kilometer resolution. They cannot resolve the submesoscale fronts and eddies that pull surface water downward. We measured that missing process in two independent high-resolution ocean models: at open-ocean fronts and deep-convection sites, 16 to 38 percent of the treated water is subducted below the winter mixed layer before it can equilibrate with the atmosphere, and the atlases resolve essentially none of it. That 16 to 38 percent is the fraction of surface water subducted at fronts, measured as passive tracer. Translated through the equilibration timescale and applied globally as a regime map, it implies current atlases over-count near-term efficiency by of order 10 to 20 percent, and more in the subpolar and Southern Ocean. It is a horizon shift, not a permanent loss, but the horizon is the whole point of a credit.

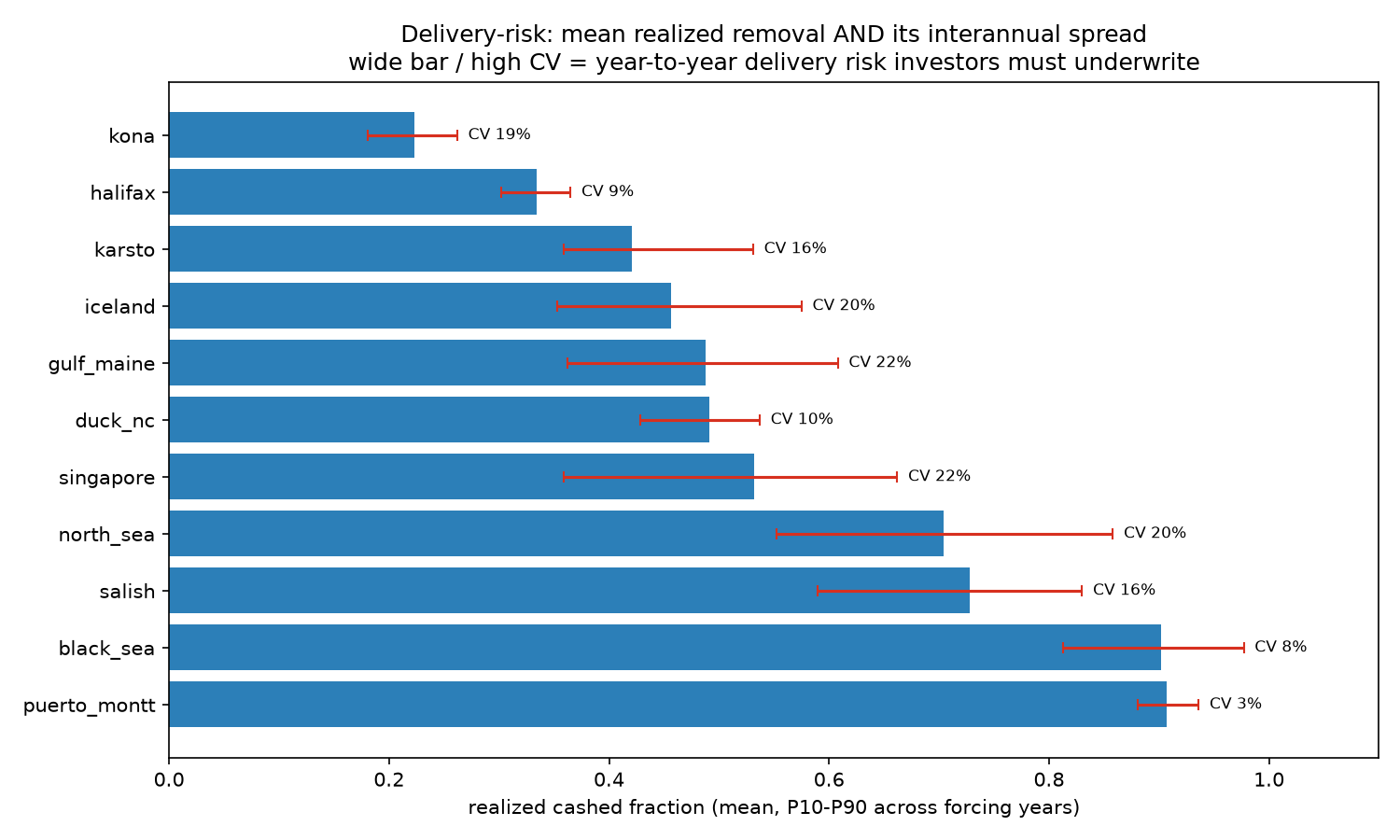

Second, the removal that does happen is unforecastable year to year from the state of the ocean. Cross-validated against climate indices, the predictive skill is near zero. You cannot underwrite a vintage on a model of the ocean, because the model cannot tell you what a given year will deliver.

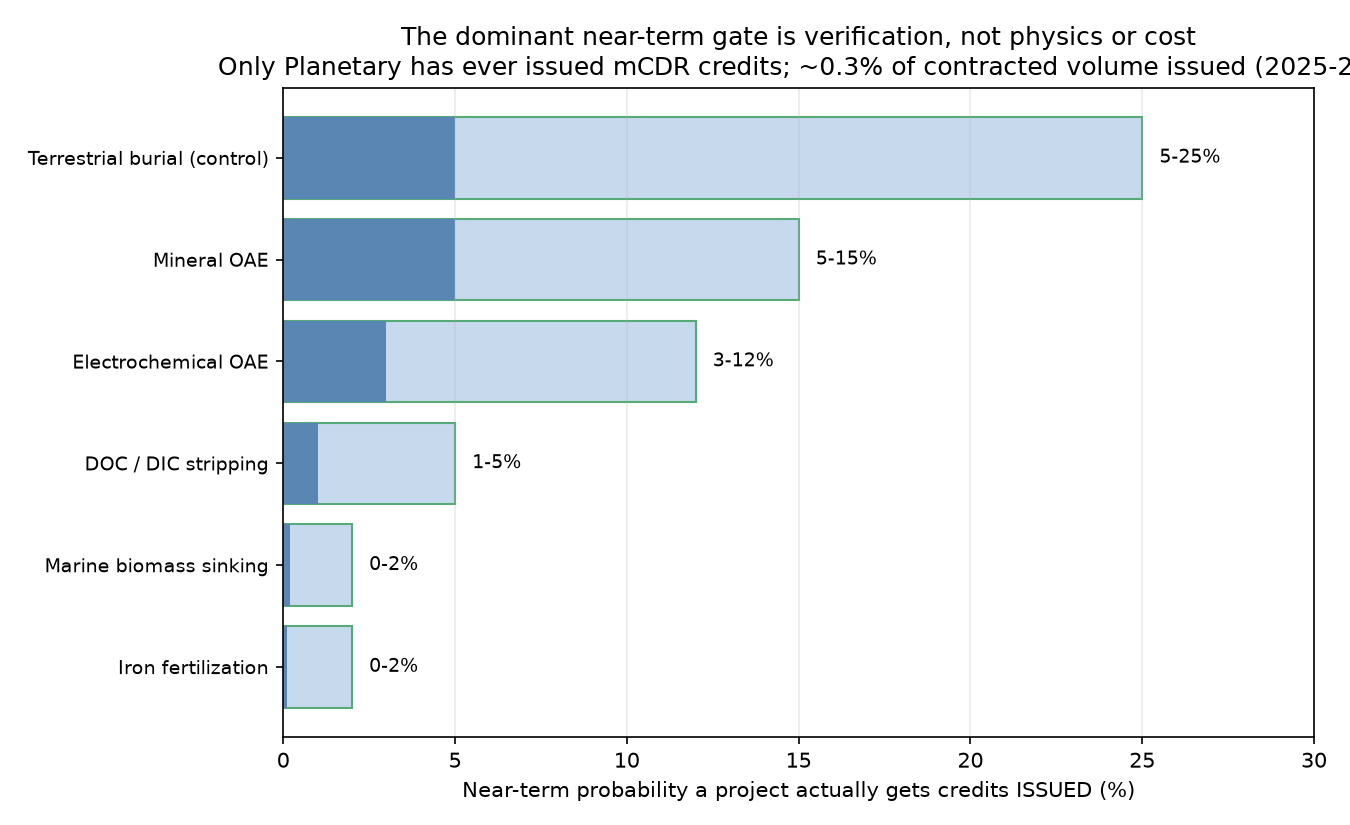

Third, the market record already reflects both. Of the ocean-CDR tonnes contracted to date, a fraction of a percent has been physically realized on the crediting horizon. The funnel from contracted to issued to physically realized is steep, and every step of it is a verification problem, not a chemistry or cost problem.

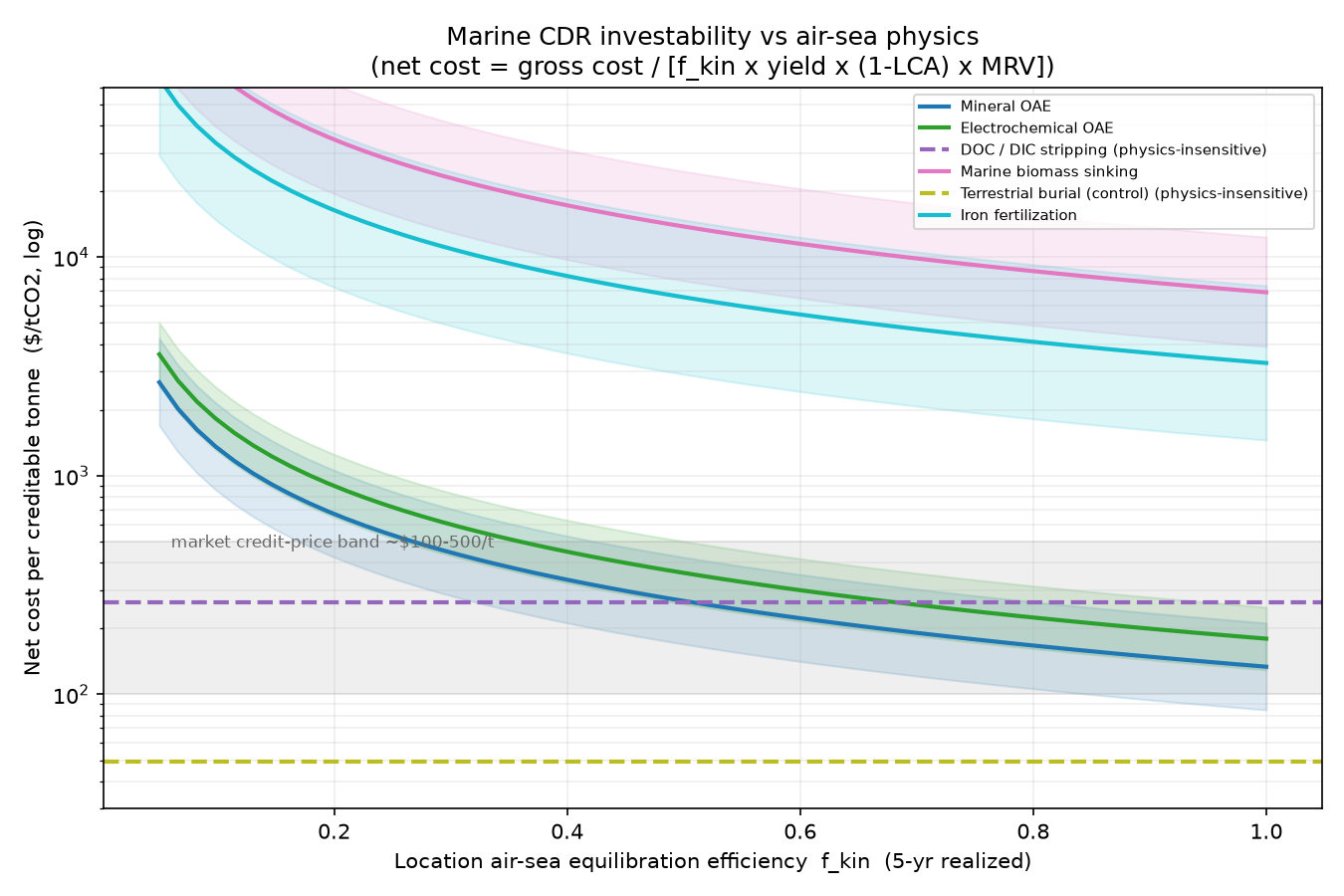

The same physics is also a method screen. Marine carbon removal is a taxonomy, not one thing. Alkalinity enhancement and direct ocean capture depend on air-sea equilibration; iron and nutrient fertilization, macroalgae cultivation and sinking, and artificial upwelling depend on biological fixation and physical export to depth. Submesoscale subduction cuts against the first family, because it strands water before it can gas-exchange, and it can cut for the second, because it is part of the export pathway. So the right diligence question is not "is this ocean CDR." It is "which physical control governs this method, and can the developer measure the quantity that governs it." For an equilibration-dependent method, that is realized surface uptake; for a biological method, it is export depth and permanence. That question is missing from the chemistry-and-cost screens the market uses today, and it separates the bankable from the unbankable.

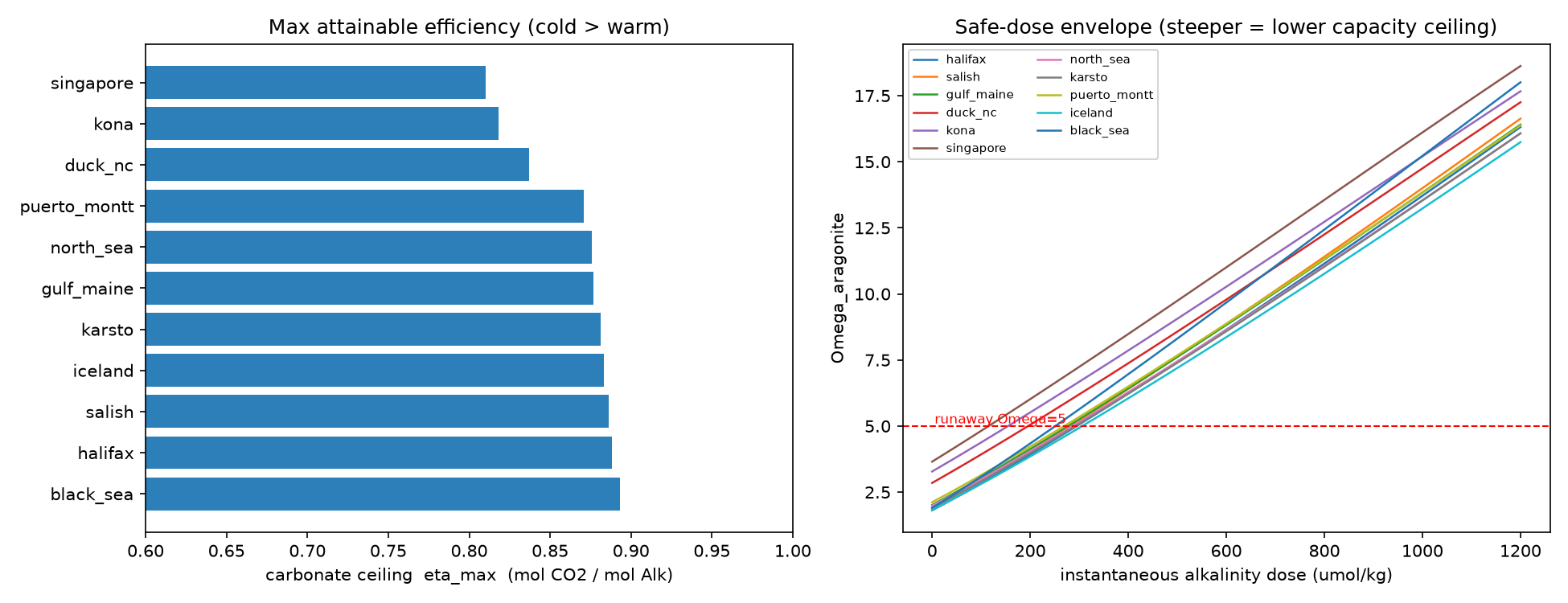

Why the biological methods do not clear, even where the physics helps them. Iron fertilization and macroalgae sinking fail on economics before verification even enters, and the export aid from subduction does not rescue them. Iron fertilization durably stores only about 2 percent of the carbon its blooms fix, because most is respired at depth or robbed from downstream nutrients, so the cost per verified tonne is high and the durability is short and contested (Ward et al. 2025, a full techno-economic assessment; Bach et al. 2025; Smetacek et al. 2012). Macroalgae cultivation and sinking carries high cultivation and sinking cost and an air-sea re-equilibration penalty that hands much of the nominal removal back to the atmosphere, so only a fraction of the gross is durable (Hurd et al. 2024; Coleman et al. 2022; Bach et al. 2021). In our reduced-form screen the two sit near 460 and 1,100 dollars per tonne with near-term issuance under 2 percent, uninvestable at any price up to 500 dollars per tonne regardless of siting. The recent science reaches the same verdict from its own side: natural ocean-biology uptake will not deliver credible carbon credits at the scale being sold (Bach, Williamson, House and Boyd 2025). The biological family is out on realized efficiency and cost, not on the subduction physics, which is exactly why a physics-aware screen separates it from alkalinity enhancement rather than lumping all ocean CDR together.

The investment consequence is a positive thesis, not a short. Value accrues to whoever can measure and verify realized removal, not to whoever deploys the most alkalinity or finds the cheapest site. Three positions follow.

- The measurement and verification layer itself. In-situ sensing, autonomous platforms, and the data and attribution stack that turns unverifiable tonnes into bankable ones. This is the pick-and-shovel layer of the entire sector, and it is undercapitalized relative to deployment.

- Measurement-native developers. Operators who build MRV in from the first design rather than bolting it on, and who can therefore sell verified tonnes rather than modeled ones. In a market that is repricing toward verification, they are the ones whose product survives contact with an auditor.

- High-resolution ocean-model and reanalysis services. The tooling that lets buyers, registries, and developers bound the resolution bias at a specific site. This is the layer that makes the first two credible.

Direct deployment is the one place to be patient. On a real-options basis, deploying alkalinity today is a bet on measurement infrastructure maturing. It flips from negative to positive expected value only once credible ex-post verification is cheap enough that a project can prove what it delivered. That crossover, not the site chemistry, is the variable to underwrite. The sensitivity is stark: at today's verification maturity the option value says wait; roughly halve the cost of credible ex-post attribution and the same sites clear. So the near-term deployment bet is really a bet on the measurement layer you could own directly.

What would change our mind. Two things. If ex-post MRV matures faster and cheaper than we expect, deployment economics turn positive sooner and the patience premium shrinks. And if a next-generation efficiency product resolves the submesoscale bias, or reliably bounds it, one leg of the mispricing closes. We are watching both. Neither is here yet.

The bottom line. The consensus is buying chemistry and cost. The physics says buy verification. The most durable positions in marine carbon removal are the instruments, the data, and the operators that make a removed tonne provable, because a market that cannot prove its product does not get to keep it.

The live Investability Screener lets any reader run a method and site through this frame: marine-cdr-screener-582896243925.us-central1.run.app. Full data and code: [Zenodo DOI]. Hold public release until preprint.

Key references. Efficiency atlas and metrics: Zhou, Tyka, Ho et al. 2024 (Nature Climate Change); Yamamoto, DeVries & Siegel 2024 (ERL); Siegel et al. 2021 (ERL, sequestration timescales). Biological methods: Bach, Williamson, House & Boyd 2025 (Nature Reviews Earth & Environment, ocean-biology credits); Hurd et al. 2024 (J. Phycology, seaweed air-sea equilibrium); Coleman et al. 2022 (Front. Marine Science, macroalgae sinking cost and additionality); Bach et al. 2021 (Nature Communications, ocean afforestation); Ward et al. 2025 (Front. Climate, iron techno-economics); Smetacek et al. 2012 (Nature, Southern Ocean iron export). Crediting and MRV: Ho et al. 2023 (State of the Planet, OAE MRV); Bach 2024 (Biogeosciences, additionality). Full reference list travels with the manuscript.